This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To help mitigate the risk of financial losses, more companies are turning to cyberinsurance. Related: Bots attack business logic Cyberinsurance, like other forms of business insurance, is a way for companies to transfer some of numerous potential liability hits associated specifically with IT infrastructure and IT activities.

Cyberinsurance definition. Cyberinsurance, also referred to as cyberriskinsurance or cyber liability insurance coverage (CLIC), is a policy with an insurance carrier to mitigate risk exposure by offsetting costs involved with damages and recovery after a cyber-related security breach or similar event.

Ironically, while many larger enterprises purchase insurance to protect themselves against catastrophic levels of hacker-inflicted damages, smaller businesses – whose cyber-risks are far greater than those of their larger counterparts – rarely have adequate (or even any) coverage.

Cyberinsurers are losing money. Their loss ratios – total claims plus the insurer’s costs, divided by total premiums earned – are now consistently above 60%, which presents something of an existential threat to the insurance industry, making cyberrisk a potentially uninsurable area due to falling profitability.

Cyberinsurance definition. Cyberinsurance, also referred to as cyberriskinsurance or cyber liability insurance coverage (CLIC), is a policy with an insurance carrier to mitigate risk exposure by offsetting costs involved with damages and recovery after a cyber-related security breach or similar event.

When considering adding a cyberinsurance policy, organizations, both public and private, must weigh the pros and cons of having insurance to cover against harm caused by a cybersecurity incident. Having cyberinsurance can help ensure compliance with these requirements. Can companies live without cyberinsurance?

That’s where cyberinsurance may be able to help. If your company has not already experienced a significant cybersecurity event, it is probably only a matter of time before it does. However, a good cyberinsurance provider can also leverage their partnerships to help your company afford better security controls.

When security fails, cyberinsurance can become crucial for ensuring continuity. Cyber has changed everything around us – even the way we tackle geopolitical crisis and conflicts. Our reliance on digital technology and the inherited risk is a key driving factor for buying cyberriskinsurance.

Cyberinsurance definition. Cyberinsurance, also referred to as cyberriskinsurance or cyber liability insurance coverage (CLIC), is a policy with an insurance carrier to mitigate risk exposure by offsetting costs involved with damages and recovery after a cyber-related security breach or similar event.

The explosion of ransomware and similar cyber incidents along with rising associated costs is convincing a growing number of insurance companies to raise the premiums on their cyberinsurance policies or reduce coverage, moves that could further squeeze organizations under siege from hackers. Insurers Assessing Risks.

Cyberinsurance is a topic that many industry professionals have an opinion on. Some believe it should be a requirement for organizations to have in the event of a cyberattack, while others might prefer to rely on their security defenses and avoid paying a costly rate. cyberinsurance rate changes.

In this regard, many have touted cyberinsurance as the knight in shining armor, the end all-be all in terms of mitigating criminals' assaults on your network. On top of this, a significant 41% of victims opted to pay the ransom, which is a difficult decision that's fraught with its own respective complexities and risks.

Interesting article discussing cyber-warranties, and whether they are an effective way to transfer risk (as envisioned by Ackerlof's "market for lemons") or a marketing trick. Our preliminary analysis suggests the majority of cyber warranties cover the cost of repairing the device alone.

Checklist for Getting CyberInsurance Coverage. As cyber criminals mature and advance their tactics, small and medium businesses become the most vulnerable because they lack the capacity – staff, technology, budget - to build strong cyber defenses. The necessity for cyber-insurance coverage.

Overall, insurance companies seem to be responding to increased demand from clients for cyber-specific insurance, and one survey found that the two things most likely to spur a purchase of cyberinsurance are when a business experiences a cyber attack and when they hear about other companies being hit by a cyber attack.

New research reveals that a record number of organizations are buying cyberinsurance policies as a tool for protecting themselves against cyberrisk. However, the cost for those policies is rising dramatically as cyberinsurance premiums soar up to 30% vs. the previous year. cyberinsurance market.

It will be unsurprising that because of this demand, insurers are particularly careful how they build their policies to minimize their risk from large cyberevents. This is especially true if the company looking for cover hasn’t taken adequate enough steps to minimize cyberrisks itself.

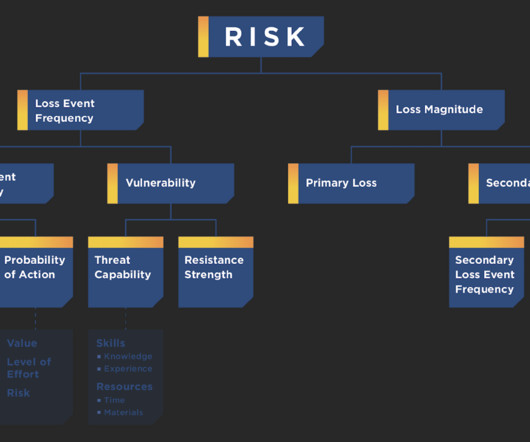

One of the important concepts about which people must be aware when evaluating their cybersecurity postures and related liabilities, but which, for some reason, many folks seem to be unaware, is the difference between first-party risks and third-party risks. First-Party Risks And Coverage. Third-Party Risks And Coverage.

Cyberrisk is an existential issue for companies of all sizes and in all industries. However, it also exposes companies to additional layers of risk. However, it also exposes companies to additional layers of risk. Real estate portfolios are uniquely exposed to cyber-physical damage risk?

Trends of cyberinsurance claims for 2020. Coalition, a cyberinsurance company, recently released a report detailing the categories of cyber attacks as well as the cause behind the attacks for the first half of 2020. 4 key takeaways from cyberinsurance industry report. Cyberinsurance works.

The timing of the attack, just ahead of a major promotional event, appears designed to disrupt critical revenue streams and shake consumer confidence. Comprehensive risk assessments To ensure your digital transformation doesn't outpace your cybersecurity, you need to conduct rigorous risk assessments and system audits.

While leveraging cyber-liability insurance has become an essential component of cyber-risk mitigation strategy, cyber-liability offerings are still relatively new, and, as a result, many parties seeking to obtain coverage are still unaware of many important factors requiring consideration when selecting a policy.

The first in-person event for RSA since the global pandemic had a slightly lower turnout than in years past (26,000 compared to 36,000 attendees). Here are some of the key trends which we observed at this year’s first marquee cybersecurity event post-pandemic: 1. Cyberinsurance becomes mainstream discussion.

AIG is one of the top cyberinsurance companies in the U.S. Today’s columnist, Erin Kennealy of Guidewire Software, offers ways for security pros, the insurance industry and government regulators to come together so insurance companies can continue to offer insurance for ransomware. eflon CreativeCommons CC BY 2.0.

Cyber is the risk to watch, according to a Financial Times article in which insurer Zurich's top executive is quoted. What will become uninsurable is going to be cyber,” said Mario Greco, CEO at Zurich, one of Europe's biggest insurance companies, in the Dec. 26 article.

First published by HelpNetSecurity — Matthew Rosenquist Cybersecurity insurance is a rapidly growing market, swelling from approximately $13B in 2022 to an estimated $84B in 2030 (26% CAGR), but insurers are struggling with quantifying the potential risks of offering this type of insurance.

(NYSE: NET), the security, performance, and reliability company helping to build a better Internet, today announced it is partnering with leading cyberinsurance companies to help businesses manage their risks online. As a result, some insurance companies have had to raise premiums to cover their costs.

In the same survey, 35 percent thought CEOs should be fined for a cyber failure, and 30 percent wanted to see a CEO lose his or her right to run any company following a serious cyberevent. And if it is, only you can take steps to get cyber right. Another 23 percent thought the CEO should face a prison sentence.

Here is Carnival Corporation's ransomware and cyber incident statement, in full: On August 15, 2020, Carnival Corporation and Carnival plc (together, the "Company," "we," "us," or "our") detected a ransomware attack that accessed and encrypted a portion of one brand’s information technology systems. And number one is cyberinsurance.

In this part of the blog series on the connection between cybersecurity and insurance, we go through a real-life situation that demonstrates how insurance policies may or may not provide you the necessary coverage in the event of a cyber-attack. A Standalone CyberInsurance Policy Isn’t Enough As discussed in our previous blog, a.

Even with ransomware costing billions of dollars in losses and cyberinsurance claims, organizations are still impacted beyond the checkbook. These attacks have driven the cost of cyberinsurance premiums higher. Cyberinsurance has become more critical to organizations to help offset the risk to the company.

The relationship between enterprises and insurers, like the cyberinsurance market itself, is evolving. Citing cybersecurity insurance as an important “component that businesses are investing in as a layer of protection,” Muldoon said no business should be operating without it. A maturing model. billion in premium.

CyberInsurance: US cyberinsurance premiums soared by 50% in 2022, reaching $7.2 Cyber Skills Gap: By 2025, there could be 3.5 million unfilled cyber security jobs, showing a big need for skilled professionals. Without any further ado, let’s have a look at the 7 most recent cyber security events.

The objective is to reassess the coverage provided by the Federal Cyber Terrorism RiskInsurance Program( TRIP) in the event of cyber-terrorist activities on the IT infrastructure hosted by public and private properties.

There is a gaping shortage of analysts talented enough to make sense of the rising tide of data logs inundating their SIEM (security information and event management) systems. This, in short, is the multi-headed hydra enterprises must tame in order to mitigate rising cyberrisks. But this hasn’t done the trick. Smart money.

Cybersecurity risks increase every year and bludgeon victims who fail to prepare properly. For those interested in a better understanding of the oncoming risks, this is the information you are looking for. It can feel like crossing a major highway while blindfolded. Many never see the catastrophe about to happen, until it occurs.

In the SecureWorld Spotlight Series, we learn about the speakers and Advisory Council members that make our events a success. He helps senior decision makers overcome cybersecurity sales objections and manages unlimited cyberrisks through rigorous prioritization. A : I own a small business called CyberRisk Opportunities LLC.

As the majority of the global Covid fog finally started lifting in 2022, other events – and their associated risks – started to fill the headspace of C-level execs the world over. Increasing demands from insurers. Here are the topics that I think will be top of mind in 2023, and what CISOs can do to prepare.

A company’s loss of control over its business practices may lead to various risks, which cybercriminals quickly exploit. However, deploying unproven artificial intelligence (AI) could result in unexpected outcomes, including a higher risk of cybercrime. Will cyberinsurance continue to be an option that organizations can rely on?

Information risk is not just a technical problem but affects the bottom line and daily activities of most businesses. It takes an organization beyond just compliance with regulations and ‘best practices’ and shows a broader overall picture of risk from different angles. How does it work?

New regulatory filings have exposed the skyrocketing costs of major cyber incidents, as big brands Clorox and Johnson Controls admitted collectively suffering more than $75 million in attack-related expenditures last year. Cleaning giant Clorox was struck by an unspecified cyberevent discovered in August 2023.

Understanding the Foundation of Risk Mitigation Implementing robust risk mitigation strategies is essential to navigating the complexities of risk-related compliance activities. But before discussing risk mitigation techniques , we must discuss the necessary prep work.

For consumers: Stay alert to potential phishing attacks or scams related to global events. Whether it’s during an election, the holiday season, a big sporting event, or a major business transaction, cybercriminals wait for the right moment to maximize damage. Cyberinsurance might also be worth looking into as an additional safety net.

His unique insights around cybersecurity-related topics shine a light on ransomware risk for organizations, government agencies, and the public. It starts with having a robust strategic plan that focuses on risk management. Testing is also an important part of risk management, and this is integral to successful risk management plans.

We organize all of the trending information in your field so you don't have to. Join 28,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content