This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Due to the complexity of the files, the Company engaged cybersecuritydata mining experts to evaluate the exfiltrated data and was recently informed of its nature, scope and validity, confirming that the data sets contained a significant number of individuals personal information associated with our clients’ end-users.”

To help mitigate the risk of financial losses, more companies are turning to cyberinsurance. Related: Bots attack business logic Cyberinsurance, like other forms of business insurance, is a way for companies to transfer some of numerous potential liability hits associated specifically with IT infrastructure and IT activities.

Ironically, while many larger enterprises purchase insurance to protect themselves against catastrophic levels of hacker-inflicted damages, smaller businesses – whose cyber-risks are far greater than those of their larger counterparts – rarely have adequate (or even any) coverage.

As we approach 2025, the cybersecurity landscape is evolving rapidly, shaped by technological advancements, regulatory shifts, and emerging threats. Below is an exhaustive list of key cybersecurity trends to watch out for in 2025. Lets explore the top current cybersecurity trends this year. The challenge?

With the average cost of a databreach exceeding three million dollars, cyberinsurance has become a necessity for SMBs. The post SMBs and CyberInsurance – Third Certainty #27 appeared first on Adam Levin. Find out more on the latest episode of Third Certainty with Adam Levin.

Cybersecurity threats are a growing menace, wreaking havoc on businesses and individuals alike. In this digital battlefield, cyberinsurance has emerged as a crucial shield, offering financial protection against databreaches, ransomware attacks, and other cyber incidents.

When considering adding a cyberinsurance policy, organizations, both public and private, must weigh the pros and cons of having insurance to cover against harm caused by a cybersecurity incident. Having cyberinsurance can help ensure compliance with these requirements.

That’s where cyberinsurance may be able to help. According to the Ponemon Institute and IBM, the global average cost of a databreach is $4.24 As the number and severity of databreaches continues to rise, organizations are recognizing that those costs are not theoretical. CyberInsurance is Booming.

So, your business has just suffered a databreach and it’s time to dig deep in your pockets to pay all the resulting expenses. Without cyberinsurance , you can expect to pay a dizzying amount of cash. Here are four ways your business can save money on its insurance. How is cyberinsurance priced?

With ransomware attacks, social engineering, and databreaches at an all-time high, terms like “cybersecurity” and “cyberinsurance” are being thrown around in conversation more than ever before. But what, in practice, do they mean – and how are the two intertwined?

Insurance firm CNA Hardy says that it has suffered a “sophisticated cybersecurity attack” that has impacted its operations, including its email system.

The rise of the cyberinsurance has largely failed to promote better cybersecurity practices among the industries they cover, according to a new report released Monday from British security think tank RUSI. However, in practice, it is still yet to be seen if cyberinsurance can fulfil this promise.”.

CISA adds Veeam Backup and Replication flaw to its Known Exploited Vulnerabilities catalog North Korea-linked APT37 exploited IE zero-day in a recent attack Omni Family Health databreach impacts 468,344 individuals Iran-linked actors target critical infrastructure organizations macOS HM Surf flaw in TCC allows bypass Safari privacy settings Two Sudanese (..)

The list of companies that have experienced databreaches in 2022 continues to grow, including Meta, Samsung, Twilio, Twitter, Uber and more. If these companies – with their large, dedicated cybersecurity teams – are vulnerable, so is every other company. The post Preparing for CyberInsurance?

The explosion of ransomware and similar cyber incidents along with rising associated costs is convincing a growing number of insurance companies to raise the premiums on their cyberinsurance policies or reduce coverage, moves that could further squeeze organizations under siege from hackers.

As the digital landscape evolves, cybersecurity remains a critical concern for businesses, governments, and individuals alike. With the advent of new technologies and rising cyber threats , 2025 promises significant shifts in the cybersecurity domain. YOU MAY ALSO WANT TO READ ABOUT: Can Cybersecurity Make You a Millionaire?

This legal turn is supported by a study conducted by BakerHostetler, which confirms that lawsuits against companies that suffer databreaches are becoming more common and may increase by the end of this year. Now the big question: Is there any benefit in filing a lawsuit against the technology service provider for a databreach?

Insurance firm CNA Financial, a prominent provider of cyberinsurance, confirmed a cyberattack against its systems, which has some concerned that cybercriminals may target policyholders. Moreover, understanding the “scope of the incident, with the type and volume of data impacted, is paramount when a cyber incident occurs.

With an ever-increasing number of cybersecurity threats and attacks, companies are becoming motivated to protect their businesses and customer data both technically and financially. The global cyberinsurance market was valued at $13.33 million — more than twice the global average of $4.35 billion in 2023 to $84.62

CyberInsurance premiums are becoming dearer and the reason for such a rise is claimed to be sophistication in attacks that are making mitigation and recovery expensive. Most companies are showing laxity in following basic cyber security hygiene, leading to a surge in cyber-attacks and databreaches.

In a report released May 20, the Government Accountability Office looked at how the private cybersecurityinsurance market has developed over the past five yearsRich Baich is global chief information security officer for insurance giant AIG. Photo by Spencer Platt/Getty Images).

With the increasing use of technology in our daily lives, cybercrime is on the rise, as evidenced by the fact that cyberattacks caused 92% of all databreaches in the first quarter of 2022. Staying current with cybersecurity trends and laws is crucial to combat these threats, which can significantly impact business development

Checklist for Getting CyberInsurance Coverage. As cyber criminals mature and advance their tactics, small and medium businesses become the most vulnerable because they lack the capacity – staff, technology, budget - to build strong cyber defenses. The necessity for cyber-insurance coverage.

The databreach of Capital One was big news, but it was also a familiar story: a major financial company with the budget and means to secure its data didn’t bother to do so, and the personal information of over a hundred million of its customers and applicants was exposed. Cloudy with a Chance of Client Error.

As organizations around the globe grapple with the consequences of databreaches, MSSPs have a unique opportunity to help their clients build and manage mature security programs and employ other necessary protections to keep their businesses safe.

Small business cyberinsurance: Is it really needed? However, according to Security Magazine , 43% of all cyberattacks target small businesses, and 60% of all small business victims of a databreach permanently close their doors within six months of the attack.

Likewise, the complexity of cybersecurity and of evaluating related risks has also translated into many insurance companies seeking to insure only large enterprises – the cost of doing business with small and medium sized business is simply not worth their time.

Cyber incidents rose 35% in 2020 with databreaches costing businesses an average of $4.24 million per year , resulting in cyberinsurance premiums jumping up by 50-100%. No doubt, cyberinsurance is a hot topic right now. It is now: how much of this insurance should you buy? Do you need it?

Every time a driver buckles up or an airbag is deployed we see the powerful influence of the insurance companies who insisted those measures become mandatory. Now, those insurers are poised to drive cybersecurity investment by insisting that organizations meet certain criteria to qualify for coverage. A maturing model.

million patients have been impacted by a health care databreach so far in 2021, a whopping 185% increase from the same time period last year where just 7.9 The attacks on our nation’s critical infrastructures, which includes our hospital systems, has resulted in government agencies showing a renewed focus on cybersecurity.”.

The cost of cyber attacks, including financial losses, reputational damage, and legal consequences, can be staggering. To mitigate these risks, businesses often invest in cyberinsurance. However, there is a powerful and cost-effective tool that businesses can utilize to reduce their cyberinsurance costs: strong passwords.

According to Accenture , more than 68 percent of business leaders feel their cybersecurity risks are increasing. That’s no surprise really, especially when considering that databreaches exposed some 36 billion records in the first half of 2020 alone.

Every year, Kaspersky experts prepare forecasts for different industries, helping them to build a strong defense against any cybersecurity threats they might face in the foreseeable future. While supply-chain is a big challenge for business right now, its cybersecurity is not merely an issue, it’s a major problem.

Here are some of the key trends which we observed at this year’s first marquee cybersecurity event post-pandemic: 1. Most customers alluded to the cybersecurity skills shortage; one of the key market drivers remains a “managed” component tailored to organizations’ response capabilities. Cyberinsurance becomes mainstream discussion.

US financial institutions see peer-to-peer fraud and other digital fraud as the biggest cybersecurity concern in 2023. CSI), followed by databreaches (23%), ransomware (20%) and a breach at a third party (15%). It was cited by 29% of respondents in a survey by Computer Systems Inc.

Frequently, the liability associated with slip-and-falls is pushed up to the owner—and within that same upstream push, so goes privacy and databreach liability. All stakeholders, including insurers, need to understand whose cyberinsurance policy responds to an incident.

One of the important concepts about which people must be aware when evaluating their cybersecurity postures and related liabilities, but which, for some reason, many folks seem to be unaware, is the difference between first-party risks and third-party risks.

Curated advice, guidance, learning and trends in cybersecurity and privacy, as chosen by our consultants. Cyberinsurance industry faces a pivotal year The cyberinsurance industry faces a pivotal year, influenced by evolving ransomware threats, regulatory changes, and the integration of artificial intelligence (AI).

First published by HelpNetSecurity — Matthew Rosenquist Cybersecurityinsurance is a rapidly growing market, swelling from approximately $13B in 2022 to an estimated $84B in 2030 (26% CAGR), but insurers are struggling with quantifying the potential risks of offering this type of insurance.

With that in mind, let’s take a look at some cybersecurity best practices for SMB IT. Sure, this might sound like something that doesn’t need to be said, but a surprising number of databreaches occur because people neglect to treat security as a priority. Carry CyberInsurance. Take It Seriously.

Following the 2016 breach, National Bank hired cybersecurity forensics firm Foregenix to investigate. “While it is fairly easy to write a policy around databreach liability, when it comes to actual intrusions and managing intrusions, it’s a wild wild west,” she said. ” .” ” .

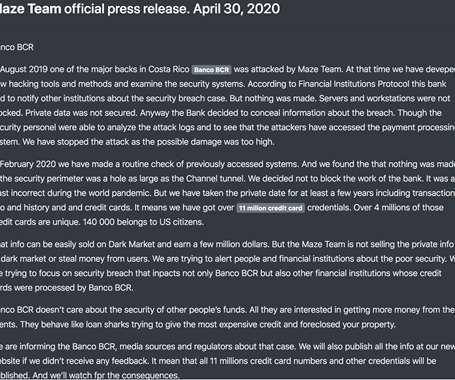

. “Just like previous data leaks, the Cyble Research Team has also identified and verified this data leak.” “As per our researchers, this data leak includes the company’s cyberinsurance documents, various contract calculations worksheets, NASA give review rules, and much more.”

For instance, 71 percent of respondents said companies shouldn’t pay ransoms to hackers, but 55 percent wanted businesses to pay a ransom if their own personal data was at risk. Preventing databreaches and implementing adequate cybersecurity safeguards was a daunting assignment even before the Covid-19 pandemic.

“The Cyble Research Team has verified this press release in which the ransomware operators state that they executed this databreach to alert people about the poor security measures being installed by these big financial institutions. ” reads a post published by Cyble.

We organize all of the trending information in your field so you don't have to. Join 28,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content