This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Global cyberinsurance premiums are declining despite an uptick in ransomware attacks, according to a recent report by insurance broker Howden. This trend reflects improved business security practices, evolving insurance industry dynamics, and changing attitudes toward cyber risk management.

The rise of the cyberinsurance has largely failed to promote better cybersecurity practices among the industries they cover, according to a new report released Monday from British security think tank RUSI. However, in practice, it is still yet to be seen if cyberinsurance can fulfil this promise.”.

Every week the best security articles from Security Affairs are free in your email box. Enjoy a new round of the weekly SecurityAffairs newsletter, including the international press.

In its modern iteration, cyber liability insurance mitigates the losses and business costs associated with cyber incidents and resulting downtime. CyberCube, a company specializing in quantifying cyber risk, estimates that the U.S. standalone cyberinsurancemarket could reach $45 billion in premiums by 2034.

But it also requires software to orchestrate data movement, backup and restore technology to ensure a current copy of data is available, and the ability to recover systems and data rapidly. This type of backup and DR technology offers RPOs measured in hours. See the Best Backup Solutions for Ransomware Protection.

The state of cyber liability insurance The topic of cyber liability insurance is full of datapoints, statistics and graphs all showing upward trajectories. What are you doing about backups? For more on this take a look at our guide: How CyberInsurance Can Be a Lifeline in Today’s Evolving Threat Landscape.

With vulnerabilities rooted in unsuspecting users, the task of preventing these attacks means both staff training and a robust email and network security system that includes a strong backup program so you have a recent copy of your data that you can roll back to. Offline Backups. Screenshot example. Ransomware facts. Version restores.

English-speaking countries, particularly the US, UK, Canada, and Australia, have well-developed insurancemarkets and higher cybersecurity awareness, resulting in higher ransomware insurance adoption. However, some cyberinsurance policies explicitly forbid ransom payments.

CEO: “ Due to complications in the market with unexpected changes in product and customer spending, we are going to announce a 20% in headcount, expenses, and capital projects for the remainder of the year.”. That $3.29, even with cyberinsurance, is still a significant hit to the organization’s bottom line.

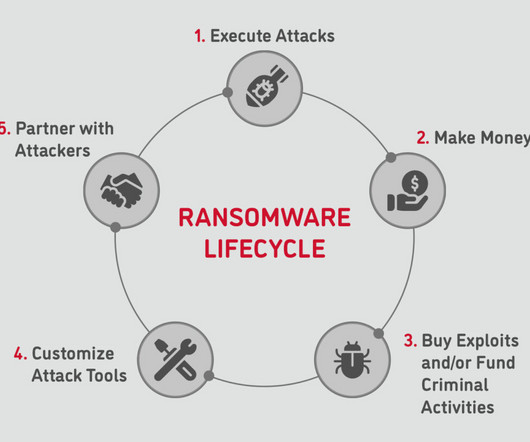

A more crowded landscape will likely drive ransomware operators to demand higher ransoms and adopt more sophisticated attack strategies to ensure their market share. This access allows newcomers to launch significant attacks with minimal investment, intensifying competition as groups rush to capture market share.

Initial Access Broker (IAB) activity increased by 16% during the reporting period, heavily targeting US-based organizations due to perceived financial capability from cyberinsurance. This includes maintaining rigorous backup policies, enhancing endpoint visibility, and ensuring all software is up to date.

One particularly unsubtle way to reduce the market for ransomware would be to expand this ban ad infinitum and legally ban payment of any ransom to anyone. It’s a little blunt to be a solution,” said Mike McNerney, chief operating officer of Resilience, which provides cyberinsurance, and a former policy adviser to the Department of Defense.

Encrypt and securely store backups offsite to protect critical data from unauthorized access or tampering. Get CyberInsurance Organizations turn to cyberinsurance to transfer risk to an organization that would cover the costs of a cyber attack, mitigating their own risk.

According to a recent market study 1 , 71% of individuals surveyed said double and triple extortion tactics have grown in popularity over the last 12 months, and 65% agree that these new threats make it tougher to refuse ransom demands. What is Double Extortion Ransomware?

Hunt and destroy or encrypt backups hosted in local and cloud networks as well as virtual machine snapshots. Average ransomware payouts are on the rise as attackers target bigger companies, specific sectors, and markets with deeper pockets. Some can’t afford not to pay, and some are covered by cyberinsurance.

As is often the case, the cost of restoring files from backups can amount to more than paying the ransom. Backups aren’t working. Restoring from backup is certainly preferable to paying the bad guys for the damage they have inflicted. Ransomware today can actually look for backup files along with user data.

We’re not marketing this as something we want to make money off of. Create backups and secure remote access, because during COVID, [the majority of attacks] were remote access credential stuffing or credential reuse, where the remote access didn’t have MFA enabled, and it was either RDP or a VPN concentrator.

Cyberinsurers are losing money. Their loss ratios – total claims plus the insurer’s costs, divided by total premiums earned – are now consistently above 60%, which presents something of an existential threat to the insurance industry, making cyber risk a potentially uninsurable area due to falling profitability.

His name is Omar Masri and he's a software engineer and also the founder and CEO of Mamari.io, which helps businesses overcome the cost and complexities of cybersecurity, preventing attacks while meeting compliance and cyberinsurance requirements. You got hacked, you’re sort of just paid, your insurance covered it.

Initial Access Broker (IAB) activity increased by 16% during the reporting period, heavily targeting US-based organizations due to perceived financial capability from cyberinsurance. This includes maintaining rigorous backup policies, enhancing endpoint visibility, and ensuring all software is up to date.

” CyberInsurance No Longer Reliable. ” Crockett said unofficial numbers indicate that only about 10 percent of such cyberinsurance claims are paid out. ” Crockett said unofficial numbers indicate that only about 10 percent of such cyberinsurance claims are paid out.

If no one paid ransom, the argument goes, there would be no market for ransomware. Backups often fail as a solution because of multiple extortion vectors or technological issues. One of the most common suggestions to deal with the ransomware scourge – also one of the most controversial – is to ban the payment of ransoms.

Obviously, organizations gotten smart to that and they started doing offline backups securing their backups differently, so that they would continue to have access and availability. They'll look at the market cap, they'll look at stock prices, they'll look at the size of the organization. By no means. VAMOSI: Should you pay?

has imposed new tariffs on Canada, Mexico, and China, setting off a geopolitical and economic ripple effect that extends beyond supply chains and global markets. Thinking a bit more widely, though, I can imagine there will be a concomitant rise in cyber espionage and attacks between groups of impacted groups in China and the U.S.

With the demand for cybersecurity professionals far exceeding supply, the market will start having openings for less qualified people. We will also see better backup practices that will help minimize or neutralize the threat of these attacks. . You’re going to have personal cyberinsurance.

We organize all of the trending information in your field so you don't have to. Join 28,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content